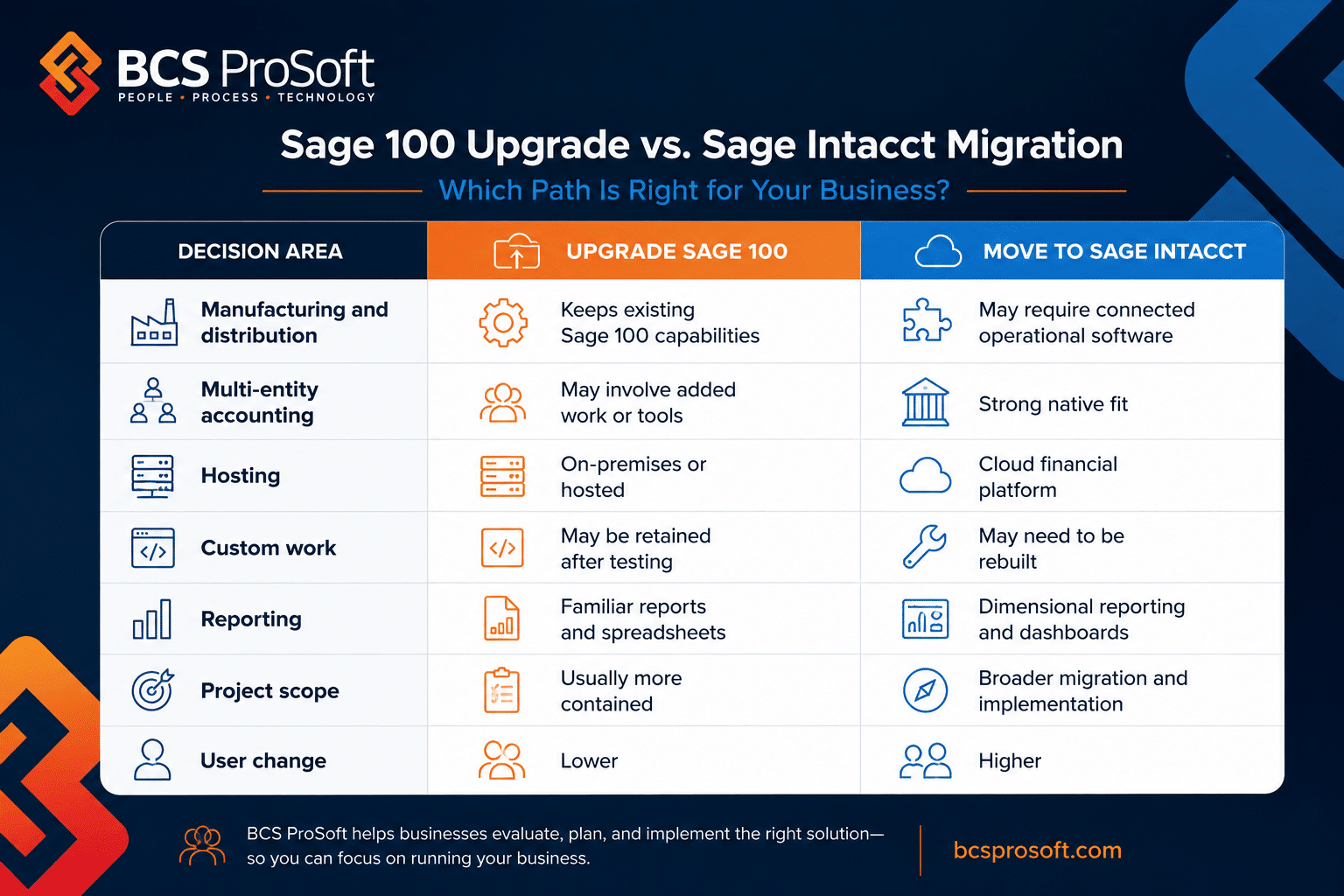

If you’ve worked in accounting, you know how important accounting accuracy is—not just for balancing the books, but for maintaining the overall health of your business. Even the smallest errors can cascade into major problems. Having seen the consequences of inaccurate reporting firsthand, I understand how easy it is for things to slip through the cracks and the headaches that come with fixing them. From simple data entry errors to compliance issues, making sure the financial statements are accurate is critical for the success and stability of any business.

In this guide, I’ll walk you through key strategies to maintain accounting accuracy, share insights from my own experience in the field, and offer practical solutions to help you avoid costly mistakes.

What Is Accounting Accuracy?

Simply put, accounting accuracy refers to the precision of your financial records and the reliability of your financial reports. It means making sure that every dollar, cent, and transaction is recorded correctly.

But it’s more than just being meticulous—it’s about building trust in your numbers so that you can make sound, informed financial decisions. Whether you’re reviewing financial statements or assessing cash flow, accurate numbers provide a clearer financial picture of your company.

Who is Responsible for Financial Accuracy in a Business?

Maintaining financial accuracy is a team effort. Different roles across the organization contribute to making sure that the numbers are right and the financial reports are reliable. But let’s break down who holds the primary responsibility and how their actions impact the accuracy of your company’s finances.

The Accounting Team

The heart of financial accuracy lies with the accounting team. These professionals handle everything from day-to-day transaction recording to preparing financial statements and reconciling accounts. Their role is to keep the books organized, check that every transaction is properly documented, and spot any inconsistencies in the numbers. An accounting team needs to stay on top of internal controls, follow established best practices, and be diligent with data entry to prevent errors.

Within the team, roles like controllers and bookkeepers take on specific duties related to keeping accounting records accurate, such as overseeing accounts payable, managing payroll, and reconciling bank statements. These roles are crucial in spotting potential inaccuracies early.

The CFO or Financial Leadership

While the accounting team handles the day-to-day tasks, the Chief Financial Officer (CFO) or financial leadership takes on the higher-level responsibility for the overall accuracy of the company’s financial reporting. It’s their job to review financial statements, interpret the data, and present it to executives, board members, or external stakeholders. They make sure that the accounting accuracy is maintained, and that the company complies with regulatory requirements and accounting standards like GAAP or IFRS.

A CFO or financial leader must also make sure that the accounting team has the right resources, such as accounting software, to improve accuracy and reduce the risk of human errors. They are accountable for signing off on financial reports, which makes them responsible for making sure those reports are a true reflection of the company’s financial health.

For companies with multiple entities, maintaining accounting accuracy becomes even more complex. CFOs should follow best practices for multi-entity reporting to ensure accuracy and consistency across all financial data.

Business Owners and Executives

Business owners and top executives may not handle the day-to-day finances, but they still play a critical role in supporting financial accuracy. Their job is to create an environment that values accuracy by providing the accounting team with the tools, software, and training necessary to keep the books in order. Executives are also responsible for approving large financial decisions and making sure that the company operates within its financial means.

They rely on the accounting team and CFO to deliver accurate financial data, which they use to make decisions about the future of the business. If the financials aren’t accurate, the whole company could be operating on faulty information.

Department Managers and Staff

Believe it or not, financial accuracy doesn’t begin and end with the finance department. Managers and staff in other departments also play a role by submitting accurate financial data, such as expense reports, invoices, and purchase orders. If inaccurate data is submitted, it causes a ripple effect that can lead to mistakes in the overall financial reporting. Department heads need to follow best practices for tracking and submitting expenses and revenue, as even small errors can throw off the bigger picture.

External Auditors and Consultants

In some cases, external auditors or financial consultants step in to help guarantee financial accuracy. They provide an objective, outside view and audit the financial processes to make sure that everything is accurate, compliant, and aligned with regulatory standards. While these professionals aren’t responsible for everyday financial management, they provide a crucial layer of oversight to make sure that there aren’t any significant errors or compliance issues that have been overlooked.

The responsibility for financial accuracy is shared across various levels within a business—from the accounting team who handle the details to the executives who make strategic decisions based on those numbers. When everyone plays their part and prioritizes accurate financial data, the entire business benefits from clearer financial insights, fewer risks, and stronger decision-making.

6 Dangers of Accounting Inaccuracies

When it comes to keeping the books straight, accuracy is everything. A tiny mistake might seem harmless, but it can snowball into major headaches, financial woes, and even damage to your business’s reputation. If you’ve been in accounting for a while, you’ve probably seen firsthand how small slip-ups can lead to big consequences. According to a recent study, businesses are losing more and more money annually due to preventable accounting errors. This highlights the importance of maintaining accounting accuracy to avoid costly mistakes.

Let’s break down why keeping things accurate is so important:

1. Compliance Risks

First up, the not-so-fun part: compliance. Messing up your financial records means you risk breaking regulatory requirements—and trust me, regulators don’t play around. You might face hefty fines, penalties, or even an audit if things aren’t accurate. No one wants to deal with that kind of heat. Whether it’s tax laws or industry-specific standards, being off by a decimal point can lead to big legal headaches.

Maintaining accounting accuracy throughout the financial close process makes it so that your business reports are reliable and compliant. For more insights on optimizing this process, explore how to optimize your financial close process.

2. Financial Mismanagement

Inaccurate accounting is like trying to drive with a foggy windshield—hard to see clearly and very risky. When your numbers are off, it’s easy to misjudge how much money you have, where it’s going, or where it’s needed. You might think your cash flow is in good shape, but inaccurate financial statements can trick you into making bad decisions, like overspending or underspending when you need to be doing the opposite.

On top of that, incorrect financial reports make it tough to know whether your business is actually profitable or bleeding money. And if you’re working with bad data, it’s only a matter of time before you’re making decisions based on numbers that don’t tell the real story.

3. Damaged Business Relationships

Ever try to explain why a payment was missed or why your financials aren’t adding up to a business partner or investor? It’s not a fun conversation. Inaccurate financials can mess up relationships with lenders, investors, or suppliers—people who rely on your numbers to make their own decisions. If your books aren’t right, it can lead to mistrust, which can cost you deals, partnerships, or even contracts. You might have the best intentions, but trust can be hard to rebuild once it’s broken.

4. Audit Trouble

No one likes an audit, but if your books aren’t right, you’re practically inviting one. Whether it’s from tax authorities or an external audit, inaccuracies tend to throw up red flags. And when auditors start digging, they can find even more issues, leading to even bigger problems. Trust me—spending weeks or even months scrambling through old records, trying to fix mistakes, isn’t something you want to deal with.

Worst case? You might end up restating financials, which can damage your business’s reputation and affect your standing with investors or regulators. Plus, it’s costly. Time is money, and audits eat up both in a big way.

5. Lawsuits and Legal Trouble

Imagine telling your investors one thing, only to find out later that your numbers were way off. That’s a quick way to end up with legal action on your hands. Stakeholders who suffer financial losses because of bad financial reports aren’t going to be happy, and some may even take it to court.

Even if it doesn’t get that far, you might be in breach of contract with lenders, violating loan agreements, or missing debt covenants. Also, legal trouble is expensive—both in terms of money and time spent dealing with it.

6. The Business Itself Can Suffer

Finally, let’s talk about the worst-case scenario: the survival of your business. When your books aren’t right, it’s like flying blind. You don’t know where your money is, where it’s going, or how to fix it when things go wrong. If this happens long enough, it can push your business toward bankruptcy. And, honestly, no one wants to be that company that couldn’t keep its finances in order.

All these risks boil down to one simple truth: accuracy in accounting isn’t just a “nice-to-have.” It’s a must. Getting it right protects your business, keeps you in good standing with partners and regulators, and helps you make the best decisions for the future.

7 Tips for Maintaining Accounting Accuracy

Accuracy in accounting doesn’t come from tools alone—it’s built on solid habits, discipline, and consistency. Effective methods exist that keep finances in check and prevent issues before they grow. Here’s a closer look at strategies that help maintain accounting accuracy.

1. Put Strong Internal Controls in Place

Strong internal controls form the backbone of any accurate accounting system. This involves setting up processes to catch errors and prevent fraud. Key elements include:

- Approval processes: Every transaction requires a second set of eyes before it goes through. Whether it’s expenses or invoices, these approvals create an extra layer of review to help avoid mistakes.

- Segregation of duties: One person handling multiple aspects of a transaction increases the risk of errors. By dividing responsibilities, mistakes or misreporting can be caught early.

- Regular audits: Internal audits or external reviews provide an opportunity to verify that financial practices are consistent and correct.

These measures keep things in check and highlight potential areas for improvement. Automation not only strengthens internal controls but also speeds up the financial close process, reducing manual errors.

2. Reconcile Your Accounts on a Regular Basis

One simple practice for maintaining accounting accuracy is reconciling accounts regularly. Comparing bank statements with internal financial records helps identify discrepancies, whether they stem from missing transactions or unauthorized activity.

Regular reconciliation of bank statements with internal financial records is crucial for maintaining accounting accuracy. Following best practices for bank reconciliation helps catch discrepancies early and makes sure your financial reports stay reliable. Setting a schedule for this process, such as monthly or quarterly, keeps everything accurate and up to date.

3. Train Your Accounting Team

Accurate accounting relies on a knowledgeable accounting team. Training helps make sure team members understand not only the best practices but also how to properly use accounting software. Key areas to focus on include:

- Accounting standards: Proper training in accounting standards such as GAAP or IFRS helps the team keep financial reporting in compliance.

- Detailed reviews: Encouraging team members to double-check their work can reduce the risk of small errors slipping through.

A well-trained team catches discrepancies early, contributing to the accuracy of the company’s financial records.

4. Maintain Detailed and Organized Records

Good accounting starts with detailed documentation. Keeping detailed and organized records for every financial transaction is key to maintaining accounting accuracy. This includes invoices, receipts, contracts, and other related documents that support the numbers on your financial statements. By having proper records, auditors, accountants, or managers can easily trace back through the transactions to verify accuracy.

Organized records simplify the process of verifying data and make financial reviews or audits far more straightforward. It helps to develop a consistent filing system so that everything is easy to access.

5. Conduct Regular Financial Reviews

Regular financial reviews play a vital role in maintaining accounting accuracy. Set aside time each month or quarter to go over financial reports with the team. These reviews help catch discrepancies before they become larger problems. It’s essential to go beyond surface-level reviews, digging into the details of revenue, expenses, and other key areas. The goal here is to stay proactive, identifying small issues before they escalate. Reviews also provide an opportunity to assess whether current controls and processes work as intended.

Regular reviews and using a comprehensive year-end close checklist help guarantee that all financial documents and reports are in order, avoiding errors and ensuring compliance with regulations.”

6. Focus on Accurate Data Entry

Accurate data entry stands at the foundation of accurate financial reporting. Even the best systems fall short when fed incorrect data. Focusing on good data entry practices avoids costly mistakes down the line. Encourage team members to double-check their work and use automation where possible, like for financial close processes. Reducing reliance on manual data entry significantly cuts down on errors.

Proper training, clear processes, and a focus on detail help avoid missteps. It’s always worth the extra time to verify that the data being entered is correct since even a minor mistake can create major problems.

7. Leverage Accounting Software for Accuracy

Accounting software plays a huge role in improving accounting accuracy. With the right tools, you can automate many of the repetitive tasks that lead to errors—like data entry or invoice processing—and focus more on analyzing financial reports and making informed decisions. Here are just a few ways how:

- Automated calculations: By automating calculations, the risk of human errors drops significantly, guaranteeing more precise reporting.

- Real-time financial tracking: Software like Sage Intacct provides real-time tracking of transactions, delivering accurate and consistent financial reports that align with your internal controls.

- Financial Statement Preparation: Using software like Sage Intacct simplifies financial statement preparation. Learn more about how to streamline financial statement preparation to make this process even more efficient and accurate.

Sage Intacct is a great option for businesses looking to improve their financial processes. However, it’s important to note that the success of implementing any software depends on how it is used. It’s crucial for businesses to have a clear understanding of their objectives and goals in order to properly utilize the features and tools offered by Sage Intacct.

Conclusion on Accounting Accuracy

Maintaining accounting accuracy is an ongoing effort, but it’s one that pays off in the long run. By implementing strong controls, leveraging accounting software, and training your team on best practices, you can significantly reduce the risk of errors and make sure that your financial reports reflect the true health of your business.

Whether you’re an in-house accountant or a CFO, these strategies can help you build a stronger financial foundation and keep your accounting records accurate and up-to-date. Remember, using the best financial close software not only ensures accurate financial reports but also helps streamline financial processes for your accounting team. If you are ready to learn more about how Sage Intacct can help you improve your financial accuracy contact us today.

Key Takeaways

- Accounting accuracy is essential for maintaining a clear financial picture, informed decision-making, and staying compliant with regulatory standards.

- Strong internal controls, such as approval processes and regular audits, are vital for preventing errors and ensuring accurate financial reporting.

- Regularly reconciling bank statements with internal records helps catch discrepancies early and keeps financial data accurate.

- Utilizing accounting software like Sage Intacct can reduce errors through automation and real-time tracking, but oversight and regular reviews are still necessary.

- Training your accounting team and keeping detailed, organized records are crucial steps in maintaining accuracy and supporting the overall financial health of the business.

Frequently Asked Questions

What is the definition of financial accuracy?

Financial accuracy refers to the precise recording, reporting, and management of a company’s financial transactions. It ensures that all financial documents, including accurate financial statements, reflect the true financial position of the business. This accuracy is crucial for making informed decisions, maintaining regulatory compliance, and ensuring transparency within the company’s finances.

What is data accuracy in accounting?

Data accuracy in accounting refers to the correctness and reliability of financial data entered into the system. It involves making sure that every transaction is recorded properly, following established standards and practices. Data accuracy supports fast and accurate accounting by ensuring that financial reports and statements are based on real, error-free data, which helps the business maintain a healthy financial management system.

What is an accurate concept of accounting?

An accurate concept of accounting means adhering to principles and practices that guarantee the integrity of financial statements. It involves systematically recording and verifying financial transactions to ensure that they are complete, timely, and error-free. This concept underpins the reliability of a company’s financial reports and is essential for sound financial decision-making and accountability