Almost one year ago, the seminal United States Supreme Court ruling in South Dakota v. Wayfair, Inc. (June 21, 2018) shattered a long-standing physical presence rule that prevented states from imposing a sales tax collection obligation on out-of-state sellers. Now, as they strive to negotiate the new sales tax landscape, many states are turning to the Streamlined Sales and Use Tax Agreement (SST) for guidance. Accounting professionals and businesses, therefore, need to understand how Wayfair and SST intersect.

Almost one year ago, the seminal United States Supreme Court ruling in South Dakota v. Wayfair, Inc. (June 21, 2018) shattered a long-standing physical presence rule that prevented states from imposing a sales tax collection obligation on out-of-state sellers. Now, as they strive to negotiate the new sales tax landscape, many states are turning to the Streamlined Sales and Use Tax Agreement (SST) for guidance. Accounting professionals and businesses, therefore, need to understand how Wayfair and SST intersect.

Wayfair recap

Most professionals who deal with sales tax have by now heard of South Dakota v. Wayfair, Inc., which grew out of South Dakota’s attempt to impose a sales tax collection obligation on out-of-state sellers with economic activity — but no physical presence — in the state.

South Dakota challenged at least two prior Supreme Court decisions holding that physical presence in a state was a requisite for sales tax collection. And it won. Physical presence in a state still establishes a sales tax collection obligation, but states can now require out-of-state sellers to collect sales and use tax based solely on economic activity in the state, or economic nexus.

Wayfair didn’t create a bright-line test like the physical presence rule to help states craft remote sales tax legislation. However, the court did highlight three aspects of South Dakota’s sales tax system that appeared designed to prevent undue burdens upon interstate commerce. These are:

- South Dakota provides a safe harbor for small businesses

- South Dakota can’t retroactively enforce its economic nexus law

- South Dakota is a member of the SST

Safe harbor. The state provides an exception for small sellers. A business establishes economic nexus in South Dakota only if it crosses the economic nexus threshold, which is more than $100,000 in sales or at least 200 transactions in the state in the current or previous calendar year.

Prospective enforcement. South Dakota began enforcing economic nexus on November 1, 2018 — more than four months after the Wayfair decision — and it cannot apply the law retroactively.

SST. South Dakota is a member of the Streamlined Sales and Use Tax Agreement, meaning it’s taken steps to simplify and modernize sales and use tax administration to reduce the burden of sales tax compliance, especially for remote sellers.

SST recap

Having been prevented from taxing remote sales on multiple occasions because of the complexity of state sales tax laws and the burdensome nature of sales tax compliance, 44 states came together in 2000 to undertake simplification measures. The result of their efforts is the Streamlined Sales and Use Tax Agreement.

The Agreement doesn’t dictate what states can and can’t tax or set specific rates. Instead, it mandates:

- A central, electronic registration system

- Consumer privacy protection

- Simplified administration of exemptions

- Simplified state and local tax rates

- Simplified tax remittances and returns

- State administration of sales and use tax collections (no self-collecting local jurisdictions)

- Uniform state and local tax bases

- Uniform sourcing rules for all taxable transactions

- Uniform tax base definitions and rules

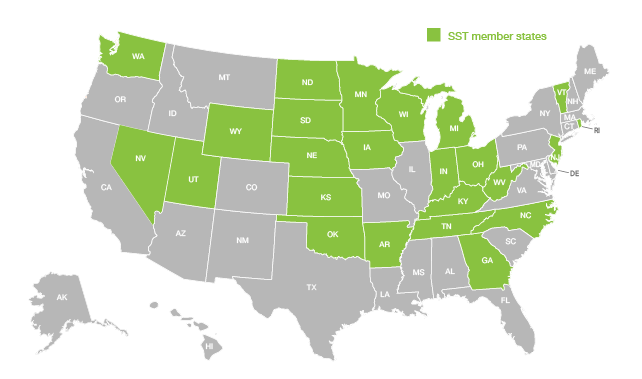

As of May 2019, 24 states have adopted the above simplification measures: Arkansas, Georgia, Indiana, Iowa, Kansas, Kentucky, Michigan, Minnesota, Nebraska, Nevada, New Jersey, North Carolina, North Dakota, Ohio, Oklahoma, Rhode Island, South Dakota, Tennessee (an associate member), Utah, Vermont, Washington, West Virginia, Wisconsin, and Wyoming. All but one — Kansas — have also enacted economic nexus.

Convergence zone: Wayfair and SST

To avoid creating undue burdens upon interstate commerce, which could potentially be found to be discriminatory, most states are looking to the Wayfair ruling and SST as they develop remote sales tax legislation. Nonetheless, complexity abounds.

What states are taking away from Wayfair

Based on the Wayfair ruling, all states with economic nexus laws are allowing an exception for small sellers. However, these exceptions vary from state to state. In California and Texas, for example, the economic nexus threshold is $500,000. In Mississippi, it’s $250,000 and systematic exploitation of the market. In Minnesota, it’s 10 or more sales totaling more than $100,000 or at least 100 separate retail sales.

Furthermore, thresholds in each state are based on different sales. Colorado and the District of Columbia include exempt sales of goods and services in their thresholds; California and New Mexico do not. Some states include digital property, some services, and some only taxable tangible personal property.

As a result of Wayfair, most states are enforcing economic nexus on a prospective basis only, and most give businesses a decent heads-up. We knew in early April that Arkansas and New Mexico would enforce economic nexus on July 1, 2019, while Texas announced in December 2018 that economic nexus would take effect October 1, 2019.

However, the New York Department of Taxation and Finance waited until January 2019 to respond to the Wayfair decision, and when it did, it announced, “Due to this ruling, certain existing provisions in the New York State Tax Law that define a sales tax vendor immediately became effective” (emphasis mine).

It takes considerable effort to establish whether a business has economic nexus in a state in the first place. Once that’s determined, the business needs to register with the tax department then commence collecting and remitting sales/use tax and filing returns according to state (and sometimes local) law.

This can be enormously impactful for companies hitting economic nexus thresholds in multiple states. SST member states strive to make it less so.

How SST can help

Any business may register through the SST to receive the benefits listed above in SST states, from consumer privacy protection to uniform sourcing rules and tax bases. Through the Streamlined Sales Tax Registration System (SSTRS), sellers can obtain the license or permit needed to collect and remit sales or use tax in all SST states, or in individual states on an as-needed basis.

Once registered, there are two paths forward: A business can manage most aspects of sales and use tax compliance itself or outsource the bulk of sales and use tax administration to a Certified Service Provider (CSP). The SST Governing Board has certified six service providers, including Avalara.

Those opting to self-manage sales and use tax benefit from the streamlining aspects of SST. For example, they can quickly and efficiently update information (e.g., change an address) or terminate registration (e.g., close a business) in all states in which they’re registered.

Sales tax compliance is further simplified for businesses that choose to use a CSP. For example, in addition to handling sales and use tax registration, Avalara provides real-time sales and use calculation, files returns, remits taxes, and more.

These services are available to any seller. For “volunteer sellers” in SST states, CSP services are subsidized by the state and provided free of charge. To qualify as a volunteer seller, a business must meet certain criteria during the immediately preceding 12-month period. These are:

- No fixed place of business for more than 30 days in the state

- Less than $50,000 of property in the member state

- Less than $50,000 of payroll in the state

- Less than 25 percent of total property or payroll in the state

- Additional criteria

Having economic nexus in a state does not disqualify a seller from obtaining volunteer status.

Wayfair beyond SST member states

SST member states certainly aren’t the only states that have adopted economic nexus. As of this writing, 41 states plus Washington, D.C., have economic legislation on the books (the laws in Massachusetts and Ohio apply to internet vendors only). Only Florida, Kansas, and Missouri have no remote seller sales tax law or rule, though Louisiana has yet to announce an effective date for its economic nexus law.

At least two non-SST states that have adopted economic nexus are emulating aspects of the SST program. Virginia’s economic nexus law requires the Virginia Tax Commissioner to simplify sales and use tax compliance for remote sellers. And the Pennsylvania Department of Revenue “is working with certified service providers to offer software and services to aid in the registration, collection, reporting, and remittance of Pennsylvania sales tax.”

Sales tax compliance is challenging, even in SST states. Sales tax software can help to make it simpler. And for volunteer sellers in SST states that use a CSP, those services are free.

Want to Learn More?

Contact us with your questions about implementing Avalara in your ERP.

________________________________________________________________________________________________

About Gail Cole: Gail began researching and writing about sales tax for Avalara in 2012 and has been fascinated with it ever since. She has a penchant for uncovering unusual tax facts, and endeavors to make complex sales tax laws more digestible for both experts and laypeople.

Sales tax rates, rules, and regulations change frequently. Although we hope you’ll find this information helpful, this blog is for informational purposes only and does not provide legal or tax advice.